The $100,000 Surprise at the Closing Table

How buyers use your roof as leverage, and how to take that leverage off the table before they find it.

🔲 The high offer isn't generosity. It's a setup. The roof is the exit.

🔲 Buyers don't guess at roof problems. They pay someone to find them, and price them at the worst number on the menu.

🔲 A hundred thousand dollar price cut starts with a two-hundred dollar inspector and a ladder.

🔲 Roof-ready doesn't mean a new roof. It means no surprises. Those are different things.

🔲 The seller who gets inspected first walks into that room with answers. The one who doesn't walks in with a number they didn't expect.

Close This. Unless Your Building is Going to Market in the Next 24 Months.

A buyer hands you a strong offer. Maybe even a little high. You take the building off the market. They put down a deposit. Then they send someone up on the roof.

And a few weeks later they're back with a new number. A hundred thousand dollars lower. And a tidy list of reasons.

This isn't bad luck. It's a move.

Good buyers run it all the time. And sellers who don't know it's coming walk right into it.

If you own a commercial building in Merrillville or anywhere across Northwest Indiana and you're thinking about selling in the next two years, this is the article to read before you list.

The High Offer is the Setup

How the playbook works, and why the roof is always the first move.

Here's how sophisticated buyers approach commercial acquisitions. And they are sophisticated, or they hire someone who is.

The high offer does one thing: it locks the building up. It pulls it off the market. It stops competing buyers from seeing it. And it starts a due diligence clock that gives the buyer sixty to ninety days to find every problem worth pricing.

The deposit makes you feel safe. You've mentally moved on. You're already thinking about what comes next.

Then due diligence goes to work.

The roof is the first stop. Always. Because the roof is the easiest, most expensive thing to point at on a commercial building. It's up there. You probably haven't seen it recently. And the replacement number, full tear-off, new system, the whole invoice, is legitimately terrifying.

So the buyer's inspector comes back with a list of seam failures, membrane degradation, ponding areas, penetrations pulling away from the flashing. Every one of those findings is real. And every one of them gets priced at the worst number on the menu.

"Our inspector found significant roof deterioration. We need to adjust the price by $100,000 to account for the replacement cost."

That sentence. Right there. That's what the playbook produces.

And if you haven't been up on that roof yourself, you have no answer for it. You're negotiating blind against someone who just paid an expert to see exactly what you couldn't.

The high offer locks the building up. The deposit makes you feel safe. The inspector makes you negotiable.

Why the Roof is Always the Easiest Target

It's expensive, it's visible, and sellers almost never know what's up there.

Think about what a buyer's inspector is looking for. Something expensive enough to justify a meaningful price reduction. Something that's genuinely the seller's problem to address. Something that can be quantified with a real contractor quote.

The roof checks every box.

A commercial flat roof replacement in Merrillville or across Northwest Indiana runs anywhere from eighty thousand to three hundred thousand dollars depending on square footage and system. That number is real. It's defensible. And it lands at the negotiating table with a quote attached.

Compare that to other due diligence findings. HVAC condition. Electrical panel age. Parking lot surface. All of them are legitimate issues. None of them produce a single-line deduction that hits six figures as cleanly as a roof replacement quote.

The roof is the biggest number they can put on one line. That's why it's always the first line.

And here's what makes it worse. Most commercial building owners in Merrillville and across NWI haven't been on their roof in years. The maintenance team handles it reactively, a leak shows up, someone goes up, something gets patched. Nobody has a current condition assessment. Nobody knows which seams are pulling. Nobody knows how much insulation saturation is up there.

So when the buyer's inspector comes down with findings, the seller has nothing to counter with. No independent assessment. No documentation. No basis to dispute the findings or the pricing.

You're not negotiating. You're surrendering with paperwork.

Most sellers haven't been on their roof in years. The buyer's inspector has been on it for three hours. That information gap is money.

Roof-Ready Isn't a New Roof. It's NO Surprises.

What sellers actually need before they list, and what they don't.

Here's where sellers make the second mistake. They hear "the roof is a problem" and they immediately start pricing a full replacement. New system. Full tear-off. The whole number.

That's not what roof-ready means.

Roof-ready means you know what's up there before the buyer does. It means you have a documented condition assessment. It means you know which problems are real and which problems the buyer's inspector inflated for leverage. And it means you've addressed enough of the real ones that you can sit across the table with answers instead of silence.

There's a significant difference between a building that needs a full roof replacement and a building with two failing seam sections and some minor penetration work. Both of them will produce a scary-sounding inspection report. Only one of them actually requires a six-figure fix.

A seller who knows the difference walks into the negotiation and says: "I had an independent assessment done. Here's what we found. Here's what we addressed. Here's the documentation." That sentence changes the entire dynamic of the conversation.

You're no longer defending. You're presenting.

The buyer can still negotiate. But they can't fabricate findings you've already addressed. They can't price problems you've already solved. And they can't use a $180,000 replacement quote as leverage when you've already documented that the actual repair scope was $22,000.

Roof-ready isn't about spending the most. It's about knowing more than the buyer's inspector before he gets on the ladder.

What an Honest Assessment Actually Finds

Core samples, infrared, seam inspection, what we look for and why it matters for your number.

When we assess a commercial roof before a sale, we're not looking for reasons to sell you a new roof. We're looking for exactly what a buyer's inspector is going to find, so you know what's coming before it arrives.

The assessment covers four areas.

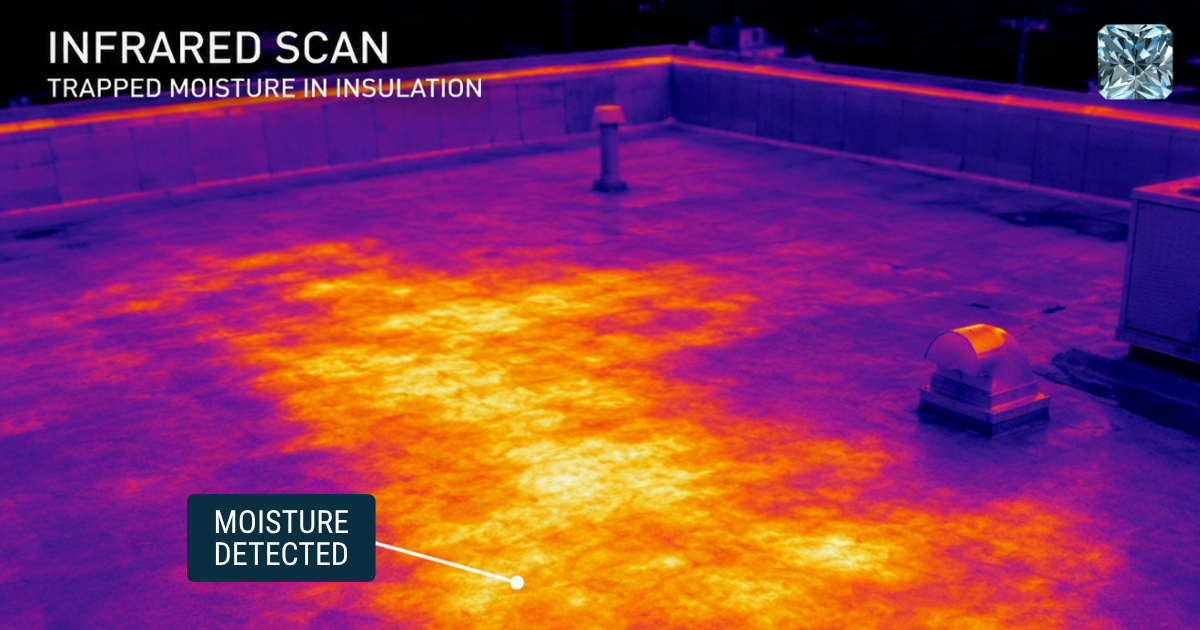

First: moisture mapping. We use infrared scanning and core sampling to identify where water has infiltrated the insulation layer. Saturated insulation is the most significant finding in any commercial roof assessment, it's structural, it affects R-value, and it's expensive to address. Knowing the saturation profile before listing tells you whether you're facing a patch-and-seal situation or a partial replacement conversation.

Second: seam condition. Every lap on the roof gets checked for adhesion, lifting, and delamination. In Merrillville and across NWI, thermal cycling accelerates seam failure faster than in stable climates. A roof that looks fine from the ground can have significant seam issues in specific zones, typically around penetrations and at drainage points where water load is highest.

Third: membrane surface condition. Chalking, surface erosion, loss of flexibility at exposed edges. These findings are real but often overstated in buyer inspections. Documentation of actual membrane condition gives you the basis to push back on inflated replacement quotes.

Fourth: penetration flashing. Every pipe seal, curb, and penetration gets checked. Flashing failures are common, relatively inexpensive to address, and frequently cited in buyer inspection reports as evidence of widespread roof failure. They aren't. They're flashing failures. Addressing them before listing removes the citation from the report entirely.

What you learn from that assessment is what the buyer's inspector is going to say. Knowing it first is the difference between negotiating and capitulating.

An independent assessment isn't a repair commitment. It's intelligence. You're buying the information the buyer's inspector would have had before you did.

Sellers who conduct independent roof assessments before listing report significantly stronger negotiating positions during due diligence. The documentation converts a subjective inspector finding into a documented and addressed condition, a fundamentally different negotiating posture.

What an Liquid Coating is the Right Pre-Sale Move

Not every roof needs replacement. Some roofs need one good answer.

Once you know what's on your roof, the question becomes: what do you do about it?

For some buildings, the answer is a targeted repair. Address the failing seams. Fix the flashing. Document the work. Go to market with a clean report.

For others, buildings with more widespread seam failure, aging membranes that are performing but showing their age, roofs that will pass inspection but invite negotiation, there's a more strategic option.

A Conklin liquid-applied coating system addresses seam failure at the source by eliminating seams entirely. Edge to edge, wall to wall, one continuous surface over the existing membrane. No more laps. No more adhesive bonds waiting to fail. And because it goes over the existing system without a tear-off, the cost is a fraction of what a full replacement would run.

For a seller, the math is straightforward. If the coating costs forty thousand dollars and it removes a hundred-thousand-dollar line item from the buyer's negotiating position, that's a sixty-thousand-dollar gain at the closing table, before you account for the deals that don't get renegotiated at all because there's nothing to point at.

You're not spending money on a roof you're selling. You're buying leverage back.

Not every building is a candidate. If the insulation is significantly saturated, coating over it creates more problems than it solves. We'll tell you that plainly if that's what the assessment finds. But for buildings with recoverable insulation and seam-based failures, which is most of the commercial inventory in Merrillville and across NWI, a pre-sale coating assessment is one of the most financially defensible decisions a seller can make.

One Assessment Changed the Entire Negotiation

One assessment. One honest answer. One closing that didn't fall apart.

A commercial owner in Merrillville came to us eight months before he planned to list. He'd owned the building for fourteen years. He had a general sense the roof was aging but hadn't had a formal assessment done.

We went up. We ran infrared. We pulled cores in three locations.

What we found: two zones of seam failure near the HVAC curbs, one area of minor insulation saturation in a low corner, and flashing pulling at four penetrations. The membrane itself was intact and adhered across roughly eighty-five percent of the surface.

His first reaction was the wrong one. He started pricing a full replacement.

We told him to stop.

The actual scope was targeted seam repair, flashing work at the four penetrations, and a Conklin coating over the recoverable surface. Total cost: twenty-six thousand dollars. We documented every finding and every repair.

He listed four months later. The buyer's inspector came back with a report. It found the same zones we'd already addressed, and our documentation showed they were resolved. The buyer had no roof-based leverage. The closing went at list price.

He didn't buy a new roof. He bought a clean inspection report. Those are very different numbers.

When the Roof Actually Does Need a Full Replacement Before Sale

Honesty first. Sometimes the right answer is the expensive one.

We're going to tell you the truth here, the same way we told it in the story above.

If the insulation saturation is above twenty-five percent, coating over it is not a viable pre-sale strategy. It seals moisture in, accelerates deck damage, and creates a liability you're passing to the buyer with documentation you signed off on. That's the wrong play legally and ethically.

If the deck has structural compromise, that conversation happens before anything else. A coating over a failing deck is not a repair. It's a disclosure problem waiting to happen.

And if the membrane is so far gone that adhesion testing shows it won't hold a surface system, a full replacement may genuinely be the right pre-sale investment, particularly if the building's price point makes the math work.

We'll give you that answer if it's the right one. We'd rather lose the coating job than sell you the wrong solution.

But in the majority of commercial buildings we assess in Merrillville and across Northwest Indiana, buildings with solid decks, recoverable insulation, and seam-based failures rather than systemic collapse, the answer is not a new roof. It's a documented, addressed, defensible condition report.

Your building has a buyer somewhere in its future. That buyer has an inspector. That inspector has a ladder and a thermal camera and a notepad full of findings.

The question isn't whether the roof comes up at the closing table. It always comes up. The question is whether you already know what's on it, or whether you're hearing it for the first time from someone who just used it to cut your number.

Let's look at it before they do.

Everything Your Real Estate Attorney Should Have Told You Before You Accepted the Offer

1. Why do buyers always seem to find roof problems during due diligence?

Because they send someone up specifically to find them. A buyer's inspector isn't a neutral party, they're looking for findings that support a price reduction. The roof is the most expensive single item on a commercial building and the easiest to price at the worst-case number. Sellers who don't have independent documentation have no basis to dispute those findings.

2. How much can a roof issue actually reduce my sale price?

In NWI commercial transactions, roof-related price reductions commonly run from twenty thousand to over one hundred thousand dollars depending on building size and the scope of findings. The buyer prices at the full replacement cost, tear-off, disposal, new system, regardless of whether replacement is actually necessary. That full replacement number becomes the opening position in the renegotiation.

3. Do I need to fix everything the inspector finds before I can close?

No. You need to know what they'll find before they find it, and you need to have addressed the legitimate issues with documentation. Minor findings that are properly disclosed and priced don't kill deals. Surprises that the seller can't explain or dispute do.

4. What does a pre-sale roof assessment actually involve?

Infrared moisture scanning to map insulation saturation, core sampling at representative locations, seam and lap adhesion inspection, membrane surface condition documentation, and flashing inspection at all penetrations. The output is a written condition report with findings, recommended scope, and cost estimates. That document is what you bring to the closing table.

5. Is a Conklin coating a credible pre-sale investment or just more money going into a building I'm selling?

It depends on the math. If the coating cost is forty thousand and it removes a hundred-thousand-dollar negotiating position from the buyer, the net is a sixty-thousand-dollar gain at closing — not counting the deals that simply don't get renegotiated because there's nothing to point at. For buildings with recoverable insulation and seam-based failures, it's frequently the highest-return pre-sale investment available.

6. What if the assessment finds something I wasn't expecting?

Then you know about it before the buyer does. That's the point. Knowing about a problem gives you options: address it, price it into the listing, disclose it proactively, or adjust your timeline. Not knowing about it gives the buyer options, specifically, the option to use it against you at the worst possible moment.

7. Is Pristine Industrial Roofing able to provide documentation that holds up in a commercial transaction?

Yes. Our assessment reports are written condition documents with findings, photographic evidence, and repair scope. They are the same type of documentation a buyer's inspector produces — which means they carry equivalent weight in a negotiation. A seller with a current independent assessment is in a fundamentally different position than a seller with nothing.

Find out what's on your roof before the buyer does.

We'll give you a written condition report and an honest answer about what it means for your sale.

Call or text: (219) 529-1995 • PristineIndustrialRoofing.com • Serving Lake County, Porter County, and Southwest Michigan.

[Get a Free Commercial Roof Inspection]

APPENDIX — SCIENCE SIDEBAR (FOR THE TECHNICAL READERS)

[Appendix A: How commercial real estate due diligence works, and where the roof fits]

[Appendix B: Commercial roof inspection methodology, what inspectors actually do]

[Appendix C: How roof replacement costs are estimated and how they get inflated]

[Appendix D: Indiana commercial real estate disclosure, what sellers are required to document]

[Appendix E: The pre-sale coating investment, financial model and return calculation]

Read other blog:

We Love Conversations

SoHelpful@PristineIndustrialRoofing.com

SoHelpful@PristineIndustrialRoofing.com